Some Stocks Worth Monitoring

Thought I’d quickly share 2 stocks I’m adding to my watch list.

Fab-Form Industries ($FBF.V)

Why am I adding this one? 4 reasons:

The company’s stock price has gotten cut in half the past year

They created a niche product that could change the way construction sites pour concrete

Rock solid balance sheet with no debt and 2/3rds of total assets in cash and short-term investments.

High levels of insider ownership

Fab-Form was started in 1986 in Vancouver B.C. and became public in 1999. It operates in the construction industry and develops and manufactures certain concrete-forming products. For example, their Fastfoot product is a laid out mesh product that helps builders pour concrete footings in order for the concrete to properly form without using excess lumber to keep it in place. They also make insulated concrete forms (ICF), which uses styrofoam to reinforce the concrete walls. They build and supply these products within the region of Vancouver. They have a new product coming out called Fast-Tube that helps guide the pouring of circular concrete walls which the CEO thinks the TAM could be a billion dollars. It competes directly with Sonotube (made by Sonoco), which uses a cardboard like cyclinder to help the concrete stay in place. Instead of the cardboard cylinder of Sonotube, Fast-Tube is a mesh, which fills up as the concrete is poured and is a much better mouse trap as it is way more efficient from a storage and transportation aspect that Sonotube.

The stock has gotten cut in half in the past year due to the decline in sales and the increased capital expenditures as the company has been investing into new products.

It’s grown from a $2-$3m business pre-Covid to peak revenues of $6.1m in 2022 and has steadily declined since. With the business being in the construction industry, it is cyclical and is affected by local housing starts, the weather (as bad weather delays construction activity) and interest rates. For only having 10 employees, it is a nice little business that is aiming to grow a lot more. The gross margins have averaged mid 30% but the operating expenses have stayed somewhat fixed over the past few years which has given them nice operating leverage which you’ll see in their increased net margins. There has been no real dilution of the shares outstanding and the company has maintained great profitability as evidenced by their ROIC and profit margins.

The company has a cash-rich balance sheet with no debt and doesn’t need much capital to operate. Management has stated that some of that cash they want to use for R&D for new products and potentially use it for marketing dollars to get the word out about these products. It’s clear they don’t need that much capital as total net working capital and PP&E is only a couple hundred thousand a year.

Richard Fearn was the president and CEO from 1986 to 2023 until he stepped aside and now Joey Fearn (his son) runs the business. Joey has been in the business for years and obviously knows the company as well as anyone. Richard owns a stake of 3.8m shares and Joey owns 192K shares as of the most recent proxy. Total insider ownership I believe is about 40% as employees own some stakes as well which creates a tight share structure and limits liquidity.

The proxy itself is a good read as the company highlights that “compensation must be performance-based”, “at least 10% of all employees’ compensation should be at performance risk”, highlighting strong ownership culture with the main focus being on building shareholder value.

On a trailing earnings basis adjusted for cash, it’s trading at about an 8x P/E multiple, 5.3x FCF multiple and 6.5 EV/EBITDA multiple.

While somewhat cheap, it’s not egregisouly cheap and to make me a bit more interested I need to see an outlined plan of what they intend on doing with their excess capital (preferably M&A or tender offer) and a return to growth. The company discloses the sale of each of their products so we can track how their new product Fast-Tube is selling.

Reitmans Limited (RET.V, RET-A.V)

Retail is one of the toughest businesses to be in. There is a lot of operating leverage but it’s also next to impossible to predict fashion trends and guess what people will want to buy. You also have to invest large amounts into inventory to sell throughout the year based on what you think your customers will like and if it doesn’t sell, one or two bad years can potentially put you under. However, there is something to be said for retailers that have been around for almost 100 years (even if this one just went through a restructuring process).

They entered CCAA (which is the Canadian bankruptcy proceedings) in 2020 and emerged in 2022. During the restructuring process, they shut down 2 unprofitable brands and let go a bunch of employees. They went from an unprofitable business to a profitable one:

I’ll admit that one of the brands they own, RW & Co., is probably my favourite clothing place. Little did I know when I came across the stock how cheap it really is:

The company is basically trading at it’s cash balance or a negative EV when not taking the lease liabilities into account. It’s at about 2x EBITDA when we factor them in. It’s also trading at a discount to reported book value of $5.6/share. They own their corporate headquarters and distribution centre in Montreal. Ernst and Young performed a liquidation analysis during the CCAA process and valued the headquarters and distribution centre at $114 million, compared to the current $88 million cost on the balance sheet. If we performed an adjusted NAV calculation and bump the PP&E up to $114 million, the adjusted NAV/share would be $6.3/share. If you were to assume last year’s EBITDA margin of 5% against $780 million in total revenues, it gets you to $39 million (this is not adding back ROU and interest depreciation. The EBITDA in the above Valuation adds it back because leases are added on to the EV). Put any type of low multiple to that, say 5x, you are at $195 million or $3.7/share, without taking into account any of the excess cash or building value.

The problem is that the controlling family, the Reitman’s, don’t seem to want to take shareholder friendly actions regarding capital allocation and corporate governance. Out of the 13.4 million common voting shares, they own 56.5% and 8% of the 38.95 million Class A non-voting shares.

Right now they own three retail brands:

1) Reitmans which is a female retail brand with 223 stores across Canada

2) Penn Penningtons which does mens and womens retail in 86 stores

3) RW & Co. which does mens and womens fashion as well in 81 stores across Canada. It operates on a similar level of Banana Republic quality/price point, just a bit above H&M.

They don’t segment their financials between brands but between retail store sales and ecommerce so there is no real way to gauge how each brand is performing.

Donville Kent sent a letter to the board in 2023 asking to eliminate the dual-class share structure, initiate a stock buyback, uplist the shares back on the TSX and have an investor relations presence by holding conference calls and having better communication to the investment community.

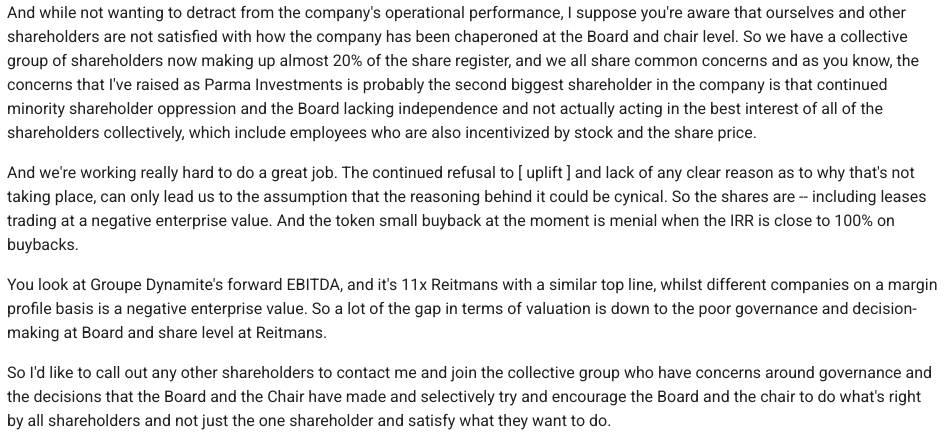

The company has taken some of their recommendations so far by introducing a stock buyback in the summer of 2024 but the amount and pace of the buyback so far has been small. And they also hired an investor relations firm last May as well. These are steps in the right direction but the stock has not gone anywhere still and you can get a sense of shareholders fustration based on their last conference call. The below is from Parma Investments on the call:

I would go even one further than what Donville Kent outlined in their letter and ask the board to form a strategic comittee to see if it makes sense to complete a sale leaseback on either one or both of their owned distribution centre and corporate head office and do a tender offer. They also just hired an outside the family CEO and gave her options with a strike price right around where the stock is trading currently.

For now, I’ll be on the lookout for any type of change to capital allocation i.e. increased speed of buybacks or corporate governance. This stock strikes me as a potential MBO opportunity if the market continues to not value it properly.

Disclosure : Added to Watchlist