A Debt Restructuring That’s Turned into a Forced Liquidation; Capital Employed Interview

Beasley Broadcast Group (“BBGI”) is now “on the clock” as it underwent an out-of-court restructuring that wiped 50% of their debt in exchange that they pay the remaining amount down by September 2027. The only way to pay this debt down without the controlling family losing the company is by liquidating assets fast. Based on the radio stations they control and other hard assets carried on the balance sheet, I estimate the stock is worth $170/share vs the current trading price of $20. This situation is high-risk, high-reward and is sized as such.

BBGI has all of the following going for it:

Prior delisting threats as the share price was under $1 and the balance sheet carried negative shareholders’ equity. This was later rectified by a reverse stock split.

The business has consistently lost money on an operating and cash flow basis for many years and recently had a $225 million FCC impairment write down.

Going concern warnings from the auditor

Related-party dealings from the Beasley family, the controlling shareholder, on real estate it uses in the business.

Excessive corporate overhead. The 3 main Beasley’s (CEO, President, COO) are paid extremely well for a microcap company. $3m in 2025 for all 3. The BOD are also paid thousands upon thousands of dollars to oversee this small microcap company. There is also a son-in-law, a daughter of the CEO and a couple of other family members who work in the business.

Operates in the FM/AM radio industry which is in secular decline.

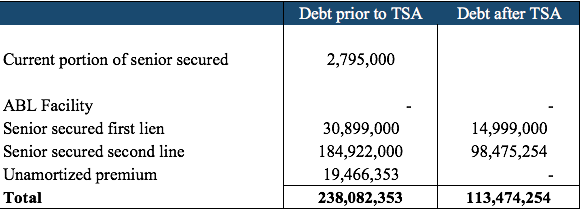

And last but not least, extremely overlevered. At one point in 2026, total debt was $238 million compared to a market cap of $6 million

So why do I think it’s interesting now? Because there was an out-of-court debt restructuring creating an equity stub that now forces the company to have to liquidate assets and pay off all of the debt. This is essentially a post-reorg equity without having to go through the bankruptcy process.

The Transaction Support Agreement Background

BBGI missed a February interest payment that started the negotiation with their lenders. In March, they announced The Transaction Support Agreement that included an exchange offer and a tender offer that took their debt down from $238 million to $113 million. Debt holders get to appoint a member to the board and 270 days after the TSA closes to appoint another member to form a strategic alternatives committee to deal with potential asset sales. They basically have until September 30, 2027 to repay all of the newly issued PIK notes and First Lien Notes. If the notes are still outstanding, the debt holders can convert the remaining amount to common shares for almost the entire company.

This investment hinges on 1) what are the assets?, 2) what are they worth? and 3) how fast can they sell them?

Business

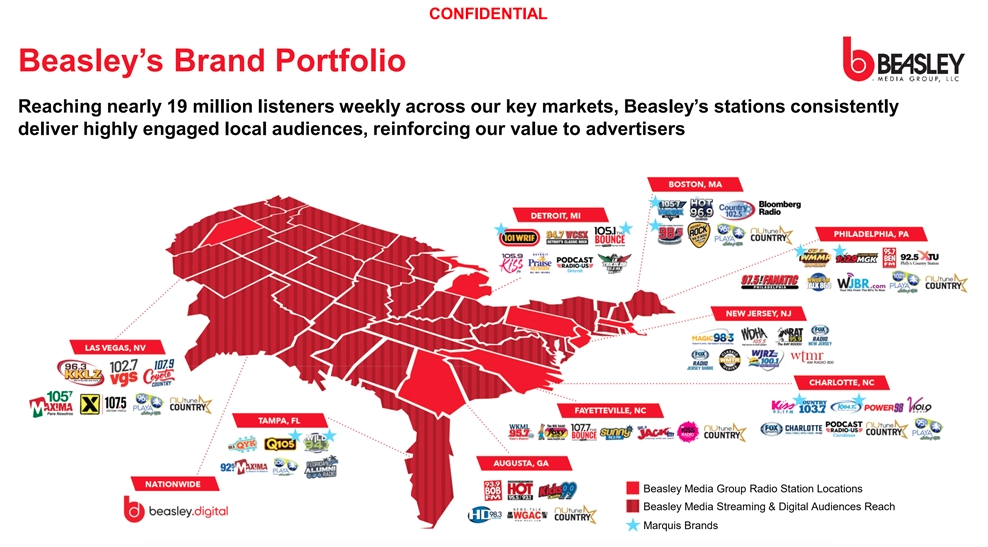

The company has a market cap of $36 million and an enterprise value of $149 million. They own and operate radio stations across the US. The industry has been in structural decline as customers listening habits have shifted to podcasts and music streaming, thereby impacting advertisers shifting dollars away from radio and to these newer products. However, they own some of the top radio stations in some large markets like Boston, Philadelphia and Detroit.

Because of the secular decline of the industry, this has led Beasley and other broadcasters to start investing in digital product offerings which has had decent success and growth the past few years. Beasley’s digital revenues of $50 million make up 25% of the company’s overall revenues currently and the segment has experienced solid growth. This has been offset by the decline in the standard on air advertising model from how the company typically makes money. The company has taken out $30 million of operating costs although not much of that has come from corporate overhead. i.e. the Beasley’s pockets.

Hard Asset Value

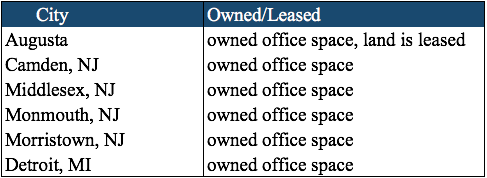

In some of the bond documents filed with the SEC over the years, there is mention of real estate owned by the company based out in California:

According to the LA County Assessor site, the land covers 124,000 square feet. Just down the street a parcel of land was sold for $65/sq.ft and according to ChatGPT, industrial property in the area has gone for $121/sq. ft.

They also own the following real estate out east that they run some of their stations out of:

The Morristown property in NJ is currently for sale according to this sales pamphlet but I haven’t been able to reach the agent to find out the listing price. On the balance sheet, land and buildings are carried at $50 million and this more than likely understates the true value since these properties have been owned for a while. I think the most conservative value would be to use that $50 million to value all of the properties.

Assessing Potential Valuation

One reason why I’m pretty bullish from the sale of assets here (besides the fact that they need to) is because earlier this year the company sold their Fort Myers stations for $18m, getting a 2.4x revenue multiple for one of their smaller markets they operated in and a market ranked 56 in the US.

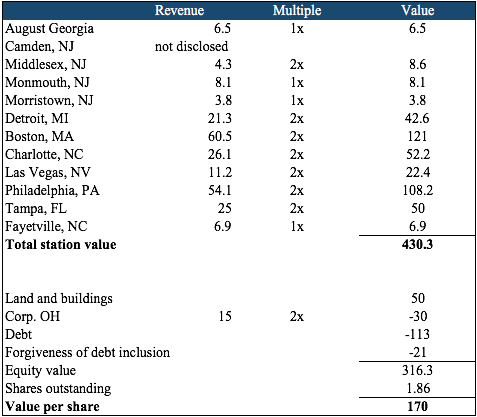

They also sold one of their Tampa stations back in September for $8 million. The M&A market for radio assets is relatively liquid even though total M&A volume has been going down year over year. Based on a white paper put out by a valuation firm last year, radio assets averaged 1.2x revenues. If I value Beasley’s higher quality assets (defined as in the top 50) using 2x and lower quality assets at 1x, the total value of the stations is $430 million.

We also have to think about the cancellation-of-debt income inclusion. Any time a corporation gets to forgive debt for less than what they took out, there is generally an income inclusion for the total dollars forgiven. In this case it would be roughly $106 million if we don’t include the unamortized premium. Taxing that at 21% would be a $22m tax bill out the door. There are certain exclusions that may apply here to not have the income inclusion liability like the insolvency exclusion where the “liabilities were greater than the assets” just prior to the debt forgiveness. I’m not a US tax lawyer and am not going to opine if they meet this exclusion. For conservative valuation purposes, I’m just going to put it into my model and assume it will have to be paid.

Putting it all together: the real estate and radio assets less debt, potential taxes and capitalizing the corporate overhead, I’m coming up with a share price of $170 vs the $20/share where it trades today.

I know it sounds crazy and I am probably missing something. If you want to include a general tax rate too for the sale of assets you can. You’d still come out with a much higher share price. I expect the equity stub to have violent moves to the upside when they start selling assets

Risks

This situation remains extremely risky due to 1) the size of the debt, 2) the year and a half period to sell the assets and 3) the debt conversion that would occur if any of the loans remaining. There is certaintly a world where they run out of time to sell enough assets to cover the debt or the prices they are getting on some of the assets might not cover it all. If bidders know that Beasely needs to sell assets they can either offer to buy at severely discounted prices or wait a year and a half and buy from the bondholders. The Beasley family would be the ultimate losers here as they’d lose their company and are heavily incentivized to fix this situation. Still, the risk of wipe out is there which is why it is a small position for me.

Disclosure: Long shares of BBGI at roughly $20.20/share with a small position.

Capital Employed Interview

Last week I was interviewed by Jon who runs Capital Employed on Substack. Here is the link.

I pitched two stocks, one of which is a new investment that I will probably write up in my Q2 letter. Enjoy!