Sato Foods Industries Co. Ltd. (2814.T) : A Negative EV Net-Net With Massive “Buybacks”

Summary

Sato ($93 million) is a small-cap net-net with similar metrics not unlike many publicly traded Tokyo-listed companies:

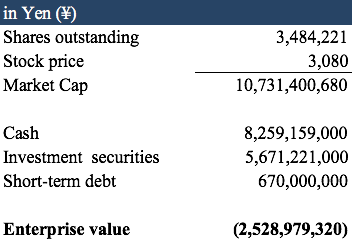

Cash and investment securities of ¥13.9B exceeds market cap of ¥10.7B

Trades at a negative enterprise value, 0.54x book value and 0.74x NCAV

Has recently started to repurchase shares over the past year

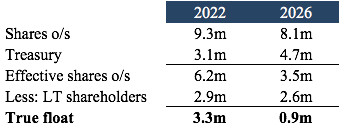

But what makes it different is the method in how they’ve managed to reduce their share count, on top of their recent buybacks. Shareholders have gifted shares and assets back to the company over the last couple of years and with the recent buybacks, Sato has been able to reduce their effective shares outstanding 45% and public float 73% in the past 4 years, all while trading under book value and at a negative enterprise value.

Business

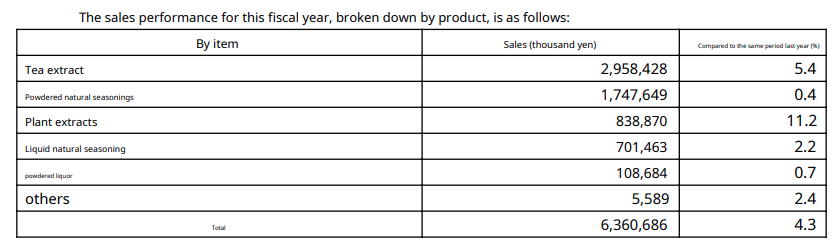

Sato’s business is relatively simple: they use their manufacturing factories to make powdered tea extracts and other natural powdered seasonings. A smaller portion of their sales are for things like powdered liquor. The tea extraction process of converting the leaves into powder is pretty scientific and Sato covers it well on their website.

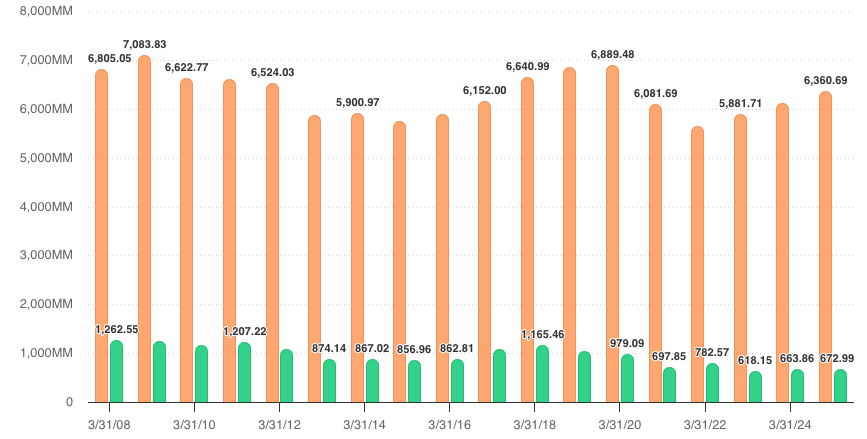

They’ve been profitable for the past 20 years (my TIKR data only goes back that far) and while margins have been decreasing the past decade, there’s been a recent uptick in sales and profits as the company has been shaking off the COVID decline of customers eating more at home than out.

Their 3 largest customers make up 35% of their sales and those top customers use Sato’s products as an input into their own products. Itoen (15.1% of sales) is the global leader in green tea products and Mitsubishi Corp. Life Sciences (10.8% of sales) has a few business lines (seasonings, extracts, etc.) that Sato’s products go in to.

Share Gifts and Repurchases

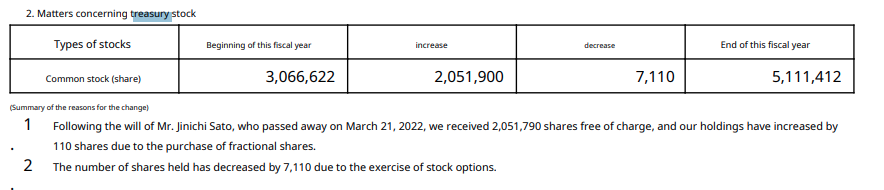

Sato has benefited from some extremely selfless shareholders recently. In 2022 when shares outstanding were 9.3m and Sato held 3.1m treasury shares, their former chairman gifted 2m shares back to the company upon his death that went right into the treasury count. Effectively reducing shares outstanding 32% without having to spend $1.

Fast forward to the summer of 2025 and another major shareholder of Sato passed. Lo and behold, this shareholder also gifted shares back to the company as well as real estate worth ¥123m yen.

On top of all of these gifted shares, Sato has started to ramp up their buybacks this past year. 5% of of their shares were bought back in September, followed by another 2% in February. They also cancelled 950K of treasury shares as well, displaying some good signs of capital allocation.

Valuation

With shares outstanding of 3.4 million and a stock price of ¥3,080, the current market cap is ¥10.8 billion. It’s net current asset value is ¥14.5 billion and book value is ¥19.9 billion so it trades at 0.74x NCAV and 0.54x book value. A lot of Japanese listed companies trade at these multiples but don’t have the unique angle of the gifts/buybacks and reduced share count with it. The operating earnings stream is going to come in just under ¥800 million this year as the company revised their earnings up recently. Sato is just dirt cheap any way you want to look at it and with shares being bought back under book, intrinsic value will only move up. Just getting to NCAV would provide upside of 35% and to book would mean upside of 85%.

I’m treating the investment securities as a part of current assets as they should be so current assets are really ¥17.4 billion and cash and investments make up 80% of that amount. I prefer my net-nets to consist mainly of highly liquid cash/investments rather than inventories or receivables as these amounts are obviously trickier to value. Sato is a stock that should be hard to lose money in unless management uses the capital for something foolish, but they’ve recently shown that’s not the case.

Why’s it Cheap

It’s Japan: There are a ton of undervalued stocks in Japan. While retail investors are starting to discover the market, it still remains undiscovered. Under 1% of shares in Sato are owed by foreign investors hence why they don’t have english financials available.

Liquidity is an issue: The shares only trade a few thousand a day. 8.1m shares outstanding, shares held by treasury are 4.7m and the top shareholders account for 2.6m which means true float is under 1m shares.

Insider alignment: Management owns next to zero shares meaning their incentive to increase the share price is nonexistent. However, they have implemented an ESOP for employees and the board that is tied to increasing the stock price in 2022 and 2024.

Opportunity for an Activist?

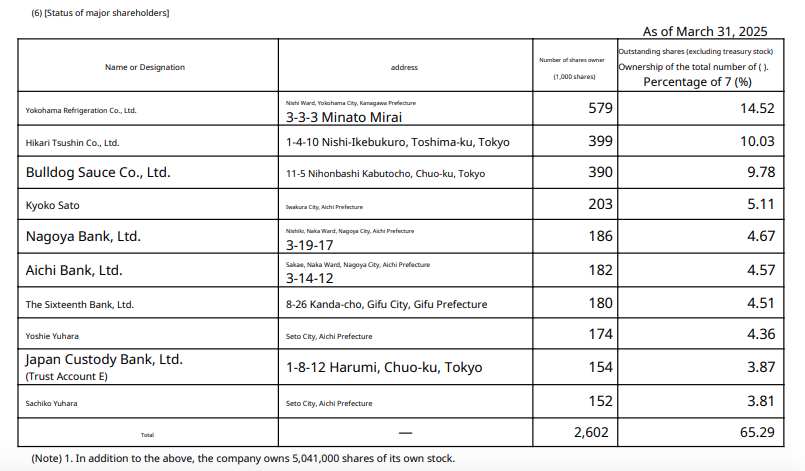

While liquidity might be an issue, an activist could potentially come in here and make some noise. It would take a few months to build a decent position, but management owns nothing and two of the top 3 shareholders are just “cross shareholders” that the TSE has been pushing for companies to eliminate.

Summary

I’m adding Sato Foods to my deep value Japan basket. There is an extreme margin of safety from a balance sheet perspective as well as an earning perspective and management has started displaying signs of smart capital allocation. Add on the unique gifts back to the company and Sato might be one of the most interesting and weirdest stock you’ll find in the public markets. This basket still represents a top 5 position in my portfolio.